Barron's has an essential cover story for fiscal catastrophe denialists among you. Fair use excerpt, with some commentary to follow (if you know the fiscal catastrophe story by heart, delight yourself by scrolling to the bottom):

As President Barack Obama and Congress continue to bicker over passing the federal budget and raising the government's debt ceiling, a report published by one of the nation's most credible agencies warns that the U.S. could face economic disaster within 25 years due to excessive government spending.CommentaryObamacare is part of the problem, but so are Medicaid, Medicare, and Social Security. The cost of these programs will mushroom as tens of millions of baby boomers reach retirement age.

The report was published on Sept. 17 by the nonpartisan Congressional Budget Office. Its most optimistic forecast shows the federal debt growing to 100% of annual economic output by 2038, from an "already quite high 73%" today. That would make the U.S. like France, which in terms of fiscal strength is none too good.

But the CBO implicitly concedes that the outcome is likely to be a lot worse than that, and so it included its "alternative fiscal scenario," which is far more realistic. It projects the federal debt will grow to 190% of the nation's annual economic output by 2038. That would make us worse than Greece today, which has a 27% unemployment rate and periodic bloody riots over its dreadful economic conditions.

A Barron's cover story on the federal debt compared the potential fiscal crisis in the U.S. to that of Greece ("Debt Crisis: Next Stop, Greece," Feb. 18). Some critics of that shocking analogy failed to notice that it did not originate with Barron's, but with the CBO itself. In its September 2013 report, the CBO stood by that analogy.

It is a truism of American democracy that politicians' time horizons rarely extend beyond the next election. That's why you have to go back nearly 15 years to find a president squarely addressing the baby-boom budget bomb. In his State of the Union address in January 1999, Bill Clinton urged Congress to seize "an unsurpassed opportunity to address a remarkable new challenge, the aging of America." With the winds of a budget surplus at his back, Clinton declared that "now is the moment for this generation to meet our historic responsibility to the 21st century."

So much for responsibility. The big opportunity slipped away, and fiscal planning has since devolved into a series of standoffs verging on defaults and shutdowns. The latest one has Washington paralyzed right now.

DEMOGRAPHICS ARE A KEY DRIVER of future spending. By 2038, there will be 79.1 million U.S. residents 65 and over, up from 44.7 million today. The working-age population, 18 to 64, will grow at a much slower rate, to 214.7 million from 197.8 million. As a result, this "dependency ratio" will plummet to 2.7 working-age people to support each senior in 2038, from 4.4 today, as illustrated by the above chart.

But since the elderly population won't begin to reach critical mass until the mid-2020s, the rising tide of red ink will be relatively contained for the next decade. Under the alternative fiscal scenario, the increase in the debt-to-economic-output ratio will be relatively modest over the next 10 years, rising just eight percentage points, to 81%, before exploding to 138% by 2033 and 190% in 2038.

The math is pretty straightforward. Retiring baby boomers are pushing up the cost of elder-care entitlements. Mainly as a result, spending will rise much faster than revenues. Deficits will therefore be incurred ever year, adding to the debt. That the federal government can no longer be expected to balance its budget, however, is not in itself the reason the CBO calls the trend unsustainable. The trend cannot be sustained because yearly deficits will be so large that the debt will grow faster than the economy's ability to pay for it.

Because most standard projections extend just 10 years, however, the media has helped stoke complacency about the budget, ignoring repeated warnings from the CBO about the misleading nature of the 10-year outlook.

The CBO's new 25-year projections should again make the message clear: The next decade is the relative calm before the coming storm. Any short-term improvement in the budget during the recent upswing in the business cycle is negligible when measured against looming long-term shocks.

The next 10 years, in other words, should be treated as an opportunity to avert the fiscal iceberg before solutions must be so Draconian that they do damage to people involved. It is difficult enough to put 50-year-olds on notice that entitlements they expect at 70 will probably not be available. To give them this bad news when they're 60 or 65 is inhumane.

Obama seems wedded to a time frame that does not even exceed his years left in office. Three days after the release of the CBO projections, the president in a speech returned to his often-repeated point that "our deficits are now coming down so quickly that by the end of this year we'll have cut them by more than half since I took office."

That boast is hollow at best, given that those deficits were all-time records. In any case, the CBO has taken all that progress into account and still deems the budget to be on an unsustainable course. If the president's Office of Management and Budget disagrees, it should explain why.

The nation might thus be likened to a family with about 10 good working years left that needs to cut spending in order to save for a rapidly approaching old age. But alas, it's a dysfunctional family incapable of rational planning. That may be one reason that rabble-rousing Republicans seek to exploit the debt-ceiling crisis as a way to reduce the debt. As Rahm Emanuel, the president's former chief of staff, once famously said, "You never want a serious crisis to go to waste. And what I mean by that is an opportunity to do things you think you could not do before."

Such as curbing the government's addiction to debt and deficits.

IN PRESENTING THE CBO REPORT at a news conference, the agency's director, Douglas Elmendorf, said the "bottom line remains the same as it was last year," clearly referring to his agency's last long-term budget projections, released in June 2012. Three things have changed since then, altering that bottom line for the better. To begin with, a tax bill was passed in January, hiking the top marginal rate to 39.6% on earnings of more than $450,000 for married couples and more than $400,000 for individuals. In addition, the CBO assumed lower spending, based mainly on slowed growth in spending on medical care. Also, gross domestic product, the denominator of the debt/GDP ratio, has been upwardly revised going back to 1929, reflecting a broader definition of GDP.

But these changes for the better have achieved very little. The CBO's alternative fiscal scenario now puts the debt/GDP ratio at 190% by 2038, as the chart on the facing page indicates, while the June 2012 version of the same scenario put the debt/GDP ratio at 190% by 2036 -- a two-year improvement.

The alternative fiscal scenario is the most realistic of those put forward by the CBO. As the agency explains, it "incorporates the assumptions that certain policies that have been in place for a number of years will be continued and that some provisions of law that might be difficult to sustain for a long period will be modified." For example, the CBO's "baseline" scenario assumes that the law requiring cuts in physicians' fees paid by Medicare will be implemented, even though Congress has rescinded these cuts every year for the past 10 years, a maneuver famously dubbed the "doc fix." The alternative fiscal scenario more realistically assumes that the doc fix is permanent.

Similarly, the alternative fiscal scenario assumes that the automatic spending cuts under the sequester, which are unpopular with Democrats and some Republicans, will be ended, although less Draconian spending caps under the Budget Control Act will continue. As Cato Institute fellow Chris Edwards, editor of DownsizingGovernment.org, says, "The CBO's alternative fiscal scenario more realistically reflects the budget culture currently prevailing in Washington."

The CBO stipulates that its "budget projections are inherently uncertain," and of course they are. They are also too plausible for a responsible government to ignore. For starters, they are driven by demographics -- the plunge in the dependency ratio -- and if demographics is not always destiny, in this case, it should be approximately right. In fact, the fiscal accident-waiting-to-happen could also occur much sooner than the CBO expects.

For example, the agency's baseline projection for real GDP growth, which determines the denominator of the debt/GDP ratio, is 2.3% per year over the next 25 years. Since annual growth has been just 1.7% since 2000, that could be far too optimistic. Also, interest costs on the debt, projected under the alternative fiscal scenario at 6% by 2038 versus 1.3% today, might be far too low. As Director Elmendorf stressed, the projected costs of debt servicing are based on past patterns, in which the debt-to-GDP ratio rose and fell.

The future debt trajectory, however, will be unprecedented, with the debt inexorably rising faster than GDP. As the market becomes aware of this dire prospect, there is no telling how high interest rates might go.

In line with the scary projections for the debt, the CBO report reiterated its previous warnings about the "risk of a fiscal crisis -- in which investors demand very high interest rates to finance the government's borrowing needs." If interest on Treasury debt reaches levels normally associated with junk bonds, interest on private-sector debt could reach levels that impair the private sector's ability to function.

Those who deny that the debt can ever be a worry for the U.S. often point out that the debt is denominated in the same U.S. dollars the Federal Reserve has the ability to print. Ergo, there needn't be defaults on that debt. But funding the debt by running the printing press could be like pouring gasoline on a fire. In fact, in his 2007 memoir, The Age of Turbulence, Alan Greenspan warned about the dangers of monetary expansion in response to the fiscal "tsunami" brought on by retiring baby boomers, and expressed the hope that the future Fed chairman would resist pressures to expand.

As Greenspan pointed out, rapid monetary expansion not only could bring price inflation, but also could cause a decline in the dollar's exchange value against other currencies. Price inflation and exchange-rate devaluation would in turn bring a plunge in the value of the dollar in which the debt is denominated, both for domestic and foreign holders of that debt. The full faith and credit backing U.S. debt would therefore be less than full, since the debt would be paid in depreciating dollars. Result: a selloff in these bonds, bringing the surge in interest rates that the CBO warned about.

While defaults on the debt would take the form of payments in depreciating dollars, defaults on entitlement programs for the elderly will probably be in terms of actual dollar cuts. But the cuts would take the form of, say, a diminished number of drugs and treatments approved for reimbursement by Medicare, or a cap on the cost-of-living escalator governing Social Security payments, especially painful as price inflation accelerates. When government tightens our belts, it rarely does so in explicit terms.

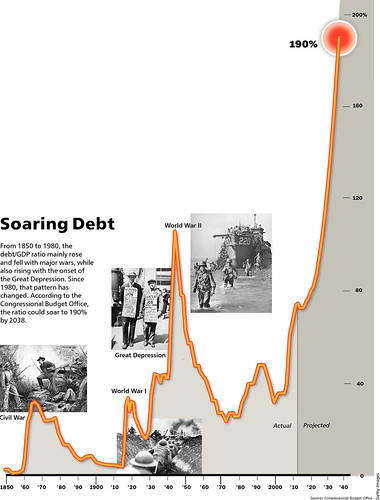

THE CHART "Soaring Debt" tells a grim story. From 1850 to 1980, the debt/GDP ratio rose with major wars -- the Civil War, World War I, and World War II -- and then in each case rapidly fell. The Korean War of the early 1950s, and the Vietnam War of the late 1960s and early 1970s, were not accompanied by increases in the ratio. Within this 130-year interval, there was only one other time the debt-to-GDP ratio rose: with the onset of the Great Depression of the 1930s.

By 1980, however, the ratio began to show a noticeable tendency to rise in the absence of a major war or major downturn. It rose in the 1980s when the tax cuts pushed through by President Ronald Reagan were unaccompanied by commensurate spending cuts. As David Stockman, budget director during Reagan's first term, has written in his recent book, The Great Deformation, "Notwithstanding decades of Republican speech-making about Ronald Reagan's rebuke to 'big government,' it never happened."

Stockman's rogues' gallery of profligate presidents also includes George W. Bush. But he exempts Bill Clinton, whose "courageously balanced budgets were the last hurrah of the old fiscal orthodoxy."....

We offer four observations that few people will enjoy.

First, when we profligately spend money on ourselves, we are destroying the standard of living of our posterity, including young people who are alive today. The money will need to be paid back, through either crushing taxation or ruinous inflation. Regardless, we are literally planning to make our own children miserable. Any time you see government at any level wasting a nickel, remember that your child will have to pay that nickel back one way or another.

Second, there is no single solution to this demographic and fiscal catastrophe. We need to reduce our spending on entitlements (particularly for future old folks who could be saving their own money or having more loving children now), we need to tilt government policy as aggressively as possible in favor of economic growth, and we need to structure our immigration decisions to support the admission of people who will bring money, brains, and ambition.

Third, we wonder if "social democratic" welfare state policies do not contain the seeds of their own destruction. Does a safety net reduce the fertility rate to the point where it makes it almost impossible to sustain the safety net? This is a question social scientists would examine closely if they were not predisposed to support social democratic welfare state policies.

Finally, we wonder if the left's denial of the American fiscal crisis is not the direct analog of the right's denial of anthropogenic global warming. Except, of course, that the American fiscal catastrophe is far more certain and will happen much more quickly.

Release the hounds.

Concerning your third point: "social democratic" welfare state policies contain far more than just the seeds of their own destruction. Were that all, it would be sufficient, and we would need only wait out the discomfort, learning the lesson for our future edification.

ReplyDeleteUnfortunately, these welfare state policies also contain the kudzu that will destroy the free nation that had reached the prosperity to let it have (for a time) those policies. There is no future in which to profit from that edification.

Eric Hines

1. Gripe, gripe, gripe--entitlements won't change significantly. It's time to attack the problem from other angles.

ReplyDeleteThe easiest way to solve the deficit problem is through the creation of a robust economy. You know how to do that. I know how to do that. But most of the people who seek political office and/or run federal bureaucracies don't know how to do that. Unfortunately, businesspeople who believe in free markets and small government won't solve the government's problems because they won't run for public office in large numbers. Why? Because they dislike government. They need to become more involved.

2. Immigration

Re: "We need to structure our immigration decisions to support the admission of people who will bring money, brains, and ambition."

We keep letting poor people into the country. Then we complain about all the poor people in the country.

The rich already can buy their way into the country. American corporations import "brains" all the time.

In the case of the poor, illegal immigrants are often more ambitious than legal immigrants.

Legal immigrants wait in line. They follow the herd.

Illegal immigrants are different. To achieve their goals, they often risk their lives to reach America. Unauthorized immigrants are brave. They are bold. They are risk-takers. They are the kind of people America needs.

Only citizens should be eligible for government jobs and government assistance. If immigrants don't like that, they should go somewhere else.

3. We need to cut our Defense budget drastically. We need to spend enough money to protect America, but we need to stop serving as the policemen of the world. The planet isn't helpless without America. Some of the smartest people in my circle of friends carry passports from other countries.

3. We need to go through the federal budget line by line, program by program, and eliminate unnecessary spending. All of it. I have seen very few companies where I couldn't reduce operating expenses by 20 percent while increasing sales, profit, and customer service. Do you think the federal government is more efficient than private industry?

4. We should think--I said "think"--about nationalizing the entire health care industry, providing U.S. Veteran Affairs-type medical care for everyone. (That's better use of tax money than spending it on free protection for people in other nations.) Yes, I know: less innovation, long waiting lines, perhaps some deaths at earlier ages. Life's full of little trade-offs.

- DEC (Jungle Trader)

Re 3 and 3: 3[sub1] should most definitely be applied to 3[sub0]. However, I disagree with giving up being the world's cop. We certainly can do a better job of that, more efficiently than we have been, but if we're not the top dog and enforcing it, our enemies will, and to our detriment and that of our friends and allies. See, for instance, Georgia and the South and East China Seas. Also, better the fight start there than in our homeland.

DeleteRe 4: We've been thinking about it, and arguing about it, since HillaryCare in varying degrees of rationality, hysteria, and polemics. A nationalized anything in our economy is a bad idea. less innovation, long waiting lines, perhaps some deaths at earlier ages are unacceptable trade-offs; we can do better.

That better begins with un-nationalizing the (separate) health care and health insurance industries--even the pre-Obamacare environment was too nationalized. With a truly free market in both industries, a requirement for plain and standardized language in health insurance policy coverages, policies able to be sold nationwide, and risk-based premiums being charged, both health care and health insurance will become vastly more accessible.

After that, and after family, friends, church, charity backups are exhausted, then the 14 or so folks who still need help will be legitimate targets of subsistence-level government (i.e., utter strangers on the other side of the country) support. Sure, plain, standardized language will be hard to achieve. Premiums for pre-existing conditions (which have most of their risk already realized) and for rare conditions will go up, but most premiums and the costs for health care itself will go down. Life's full of little trade-offs.

PS: drag the right bottom corner of the (draft) comment box. It doesn't get wider, but it gets longer. It'd be alright if there were one on the Preview box, too....

Eric Hines

1. EH: "Also, better the fight start there than in our homeland."

DeleteYeah, I remember that argument when I was a soldier during the Vietnam War: "We are fighting them in Vietnam now so we don't have to fight them in California later." We didn't win that war, and I haven't seen any Vietnamese soldiers invading the Golden State.

Today I do business with the Vietnamese, the Russians, and the (Mainland) Chinese.

2. Calvin Coolidge said, ". . . the chief business of the American people is business. They are profoundly concerned with producing, buying, selling, investing and prospering in the world."

For centuries the Swiss stayed out of other people's fights. In the 1980 movie "The Formula," the Marlon Brandon character said, "In business we are all Swiss."

"The Formula" is only a movie. But I agree wholeheartedly with the Marlon Brando character's statement.

- DEC (Jungle Trader)

P.S. I'm sorry about the numbering mistake in my comment. The copy for proofreading (preview) didn't show the entire post liked it used to do. It showed four lines at a time.

ReplyDeleteI have to laugh that any one with a sense of geology and recent global ice ages discounts the fact that the Earth in the last two million years has undergone 20 major glacial events with the average change in oceans of up to 1,000 feet and that the amount of ice still on the planet equates to 230 more feet of potential ocean waters.

ReplyDeleteWith that backdrop, who gives a rat ship about anthropogenic global warming.

The Earth itself is still in and going to be in a global warming and cooling cycle for the next 18 million years, or until Antarctica moves its behind off of the South Pole.

I currently sit in a location that was covered by 1,000 feet of solid ice a mere 10,000 years ago and will again during the next glacial epoch, expected to start in the next 10 - 20 thousand years.

The whole notion from the enviro-spiritual-wacko nut jobs that the Earth is somehow a stable but not chaotic ecosystem during an ongoing Ice Age is the lunacy that no one in the media wants to talk about - most likely because most in the media and general public are ABSOLUTELY IGNORANT that we still are in the midst of an Ice Age and the meager global changes in climate forecast over the next century are well within the margins of expectations of a climate during AN ICE AGE.

If you don't know or understand the global climate in an ice age, give thanks and homage to the current state of science education in America today.